Cephalon Pharmaceuticals (CEPH)

In December biopharmaceutical company Cephalon Inc. made the announcement that it has reduced its debt levels by exchanging a combination of cash and stock for $337 million in convertible notes. Cephalon exchanged $161.6 million of its zero coupon convertible subordinated notes due June 2008 and $175.4 million of similar notes due June 2010 for $101.6 million in cash payments and 4.3 million common shares.

The company expects to book a related $20.8 million charge in its fourth quarter.

As a results of the transactions, Cephalon reduced its 2007 outlook for basic adjusted income to $4.15 to $4.25 per share.

The company said its 2006 earnings and sales outlook remain unchanged, as does its 2007 sales forecast. In November, Cephalon projected 2006 sales of $1.66 billion to $1.68 billion and basic adjusted income of $5.10 to $5.20 per share. Sales in 2007 should range from $1.68 billion to $1.73 billion.

Also, Cephalon announced in December that FDA would likely delay a final approval decision on its drug Nuvigil for excessive sleepiness while the agency continues to investigate a case of a potentially serious skin rash seen with a related medicine. The company however reiterated it's sales forecast for 2007 and do not expect a significant effect from this delay since they expe

cted to have a "modest" launch of Nuvigil which is expected to replace Provigil once it's patent expires.

Cephalon has done a great job of managing its product life cycle by developing Nuvigil and launching it before Provigil patent expires.

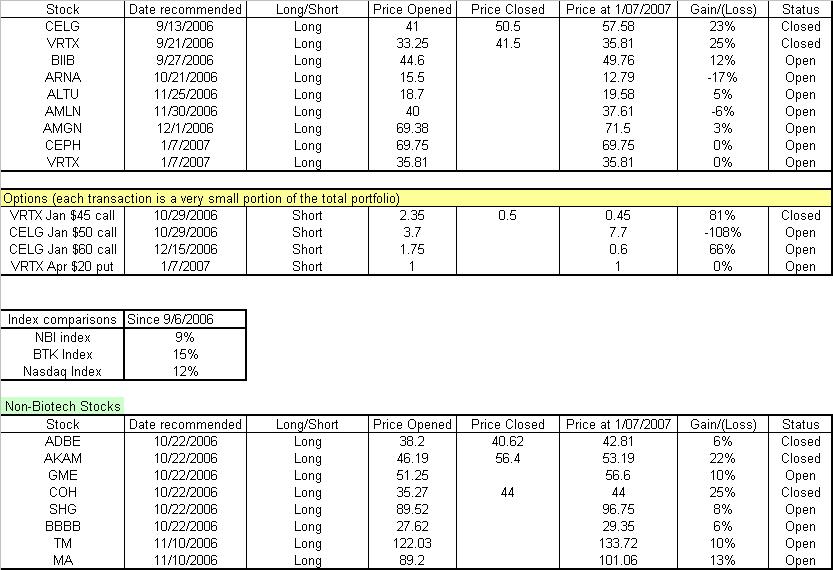

CEPH stock is currently at $69.75 and trading at about 15X 2007 expected earnings and well off of it's 52 week high of $82.92. I consider this level a great value and opening a position at these levels. The chart to the right shows a down side risk to $55 where the stock would be trading at Dirt Cheap prices. I think given the relatively safe earnings prediction as well as the new capital structure the stock has little risk of down side move given the overall sector does not take a major hit.

JMHO.