My last performance review was in April of this year. I have not been writing much recently and not due to laziness. The reason for this lack of activity was my overall skepticism of the markets. Two sharp corrections

happened this year in March and in August, from which the markets have strongly rebounded. The underlying

economy however was extremely weak and it looked like we were going into a recession induced by a crisis in the housing market. The fed however decided to reduce interest rates earlier this month to avoid a recession. I believe this was a mistake. I don't think the Fed's job was to bail out bad hedge funds, bad loan under writers and consumers who made poor decisions by making borrowing cheap again. I believe the long term effects of this act will be increased inflation, higher long maturity bonds and a collapse in the dollar. I hope I am wrong!

But the m

acroeconomy is not the

topic of this blog. I should instead talk about how this will affect Biotechnology and Pharmaceutical stocks. Since

Biotechs in general have low amounts of debt, the effect of lower costs of borrowing on profit margins will be minimal. For Big

Pharma however there will be significant increases in earnings due to lower costs of borrowing and a better foreign exchange rate due to weaker dollar.

Biotech is still a product driven not a consumer driven industry so the impact of the rate cuts will be minimal to the revenues of this industry.

If I had to sum up 2007 ( to date) for

Biotech Stocks in one word it would be UNEVENTFUL.

Charly Travers from

Motley Fool.com probably had the best prediction for

Biotech stocks in 2007. I don't have the link but he basically predicted a flat year due to lack of important product launches. Indeed the story this year was that most

Biotechs met their expectations but the lofty historical

PEs has shrunk.

Last year, I had analyzed the PE to Growth ratios of some big

Biotech names and identified

CELG (

Celgene) as the cheapest based on PEG analysis. It is interesting to visit those numbers again 12 months later to see if they tell a story. Click on the following image to see this analysis. The top table is the analysis done in 2006. The bottom table is the same analysis in 2007 and the colors show which stocks went up and down in that time.

Interestingly,

CELG is still the cheapest of these stocks with a PEG of 1.14. However, I am going with

BIIB (

Biogen Idec) and

GENZ (

Genzyme) as my picks for 2008 because they have a more diversified portfolio of products with revenues than

CELG who is dependent on Revlimid for most of its revenue. One bad earnings quarter and

CELG’s price could see a huge decline. I am most bullish on

GENZ because they have

consistently beat estimates but the stock is actually down from last year. So, If I have to make one pick for a large cap

Biotech in 2008 it is

GENZ. I also can not expect too many bad years from DNA (

Genentech) so I will recommend that as well. I don't like GILD (Gilead), according to a PEG of 2.5, they are overpriced. Finally,

AMGN (

Amgen) had a tough year. They have a great

pipleline and will make a come back but I am staying away until I see poof that things are better.

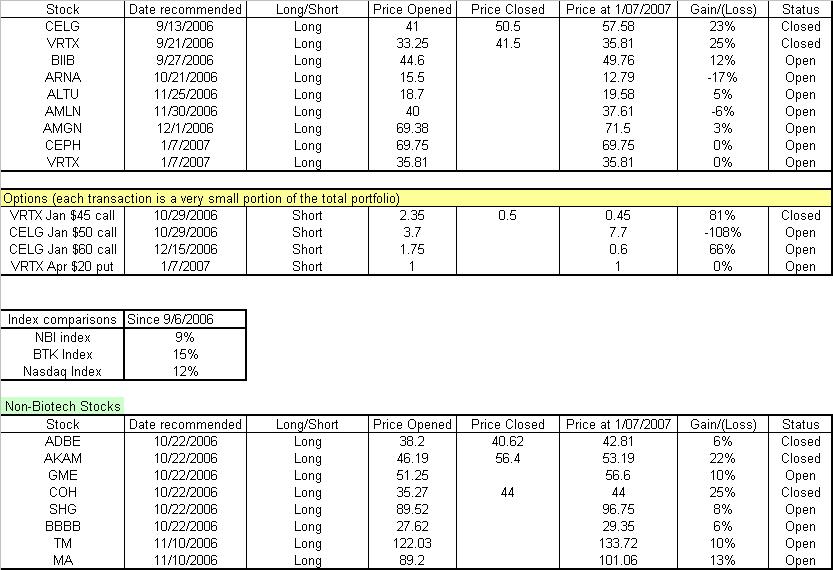

CELG is in interesting stock which affected the performance of my picks this year. The table below shows an update of my historical

biotech and non-

biotech picks.

I have highlighted some intersting results from the portfolio First, the overall return on the stock component is much lower than the two Biotech indices. In the past 12 months, my stock portfolio yielded a 10% return while NBI index had a return of 15% and the BTK (large caps) returned an impressive 25%. I blame all of this under performance on getting out of CELG too early. It was a rather costly mistake. One that I hope I will not repeat. I was also bady hurt by lack of performance in my small cap biotech names (Altus and Arena) but I like both in the long term. I should also mention that I stayed away from good small cap stocks such as ALNY (Alnylam) which would have been helpful to my returns.

I have highlighted some intersting results from the portfolio First, the overall return on the stock component is much lower than the two Biotech indices. In the past 12 months, my stock portfolio yielded a 10% return while NBI index had a return of 15% and the BTK (large caps) returned an impressive 25%. I blame all of this under performance on getting out of CELG too early. It was a rather costly mistake. One that I hope I will not repeat. I was also bady hurt by lack of performance in my small cap biotech names (Altus and Arena) but I like both in the long term. I should also mention that I stayed away from good small cap stocks such as ALNY (Alnylam) which would have been helpful to my returns.

On the bright side, the options helped me get some additional returns. In the past I was not able to quantify their impact. However, going forward I can accomplish this by calculating the return on underlying collateral required for a naked option. Trading wisely with options could improve any portfolio's return and protect against volatility so I am going to keep investing with both options and stocks.

The Non-

Biotech stocks had a much nicer return for a few reasons. This was mostly due to the fact that I was not exposed directly to any

sub prime stocks such as the investment banks, regional banks, construction or mortgage brokers. I was also helped greatly by returns in

GME (

Gamestop) and MA (

Mastercard) which I still like going

foreword. I will add shares of

GOOG(Google) and (

AAPL) for tech names as well as shares of TIE (

Titanim Metals) and COP (

Conoco Phillips) to get exposure to commodities that get helped with weak dollar. Lastly, I like exchanges

CME (Chicago Mercantile Exchange) and

NMX(

Nymex) as increased commodity and futures trading and volatility in addition to consolidation in the industry will help both exchanges.

Bottom line: 2007 was a lackluster year for

biotech sector and I look forward to a better 2008 because of increase in

product development. I expect

GENZ,

BIIB and DNA to outperform their peers. I am still very bullish on

VRTX as well.

My goal is to improve on my picks and the timing of my trades in order to beat the

Biotech indices in 2008.

Disclosure: The author holds long positions and actively trades in stocks recommended in this article and their options.

{kind=link}