Arena Pharmaceuticals, Inc (

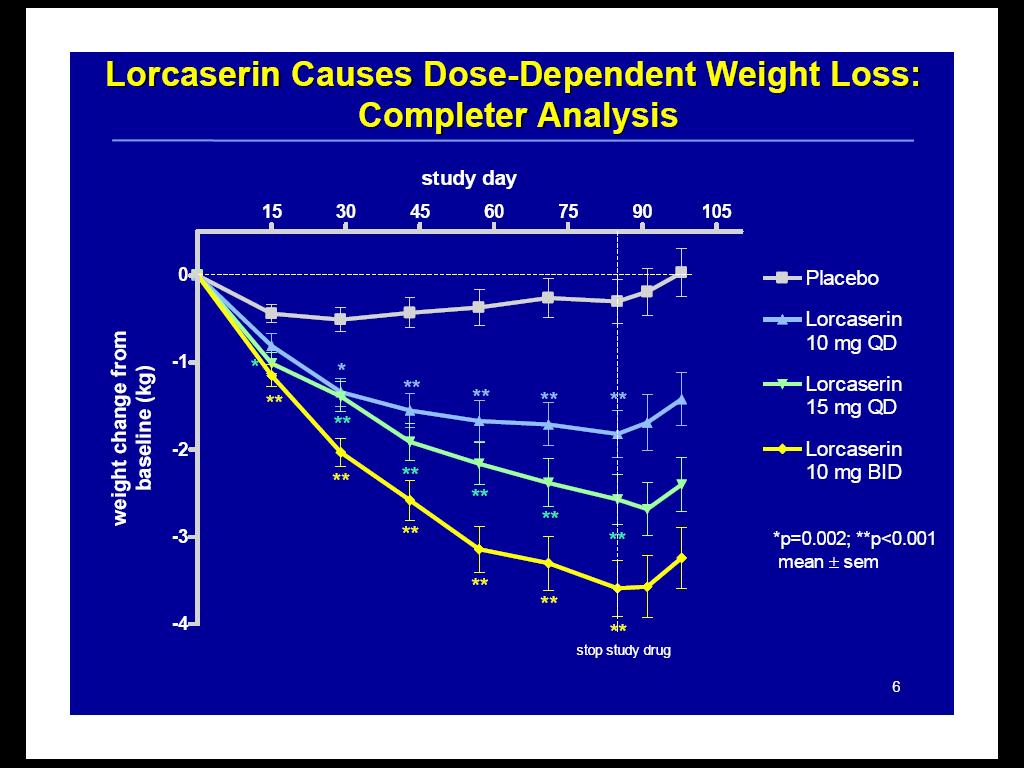

The outcome for of Arena, as a company and as a stock, depends heavily on success of Lorcaserin as an obesity drug. The market is undeniably huge and lack of good existing treatments allows for rapid market share gains. There may be future competition in form of late stage drugs in the clinic. (Sanofi’s weight loss is also in Phase III). Lorcaserin works by selectively inhibiting a serotonin receptor. I like GPCR as a class of drugs because their therapeutic and toxicityt characteristics have been well studied in the past from other drugs that have made it to the market. The phase IIb clinical trial results were quite impressive. In order to keep this article to a manageable size, I will discuss only the highlights. The attached image (click the image to enlarge) shows the efficacy results of Lorcaser in at different doses and dosing schedules compared to Placebo in a Phase II clinical trial. The drug exhibited a dose response curve (higher results at higher doses), which were significantly better than the Placebo affect. Also, once the patients discontinued the therapy, they gained some weight. This has significance because it is another proof that the results are based on the targeted action and not due to a side effect. Furthermore, chronic dosing brings more sales to the company. There were no signifant side effects or cardiovascular toxicity issues that have plagued other weight loss drugs in the past. Besides Lorcaserin, Arena has other clinical candidates (Insomnia, Diabetes) that add value to the company.

in at different doses and dosing schedules compared to Placebo in a Phase II clinical trial. The drug exhibited a dose response curve (higher results at higher doses), which were significantly better than the Placebo affect. Also, once the patients discontinued the therapy, they gained some weight. This has significance because it is another proof that the results are based on the targeted action and not due to a side effect. Furthermore, chronic dosing brings more sales to the company. There were no signifant side effects or cardiovascular toxicity issues that have plagued other weight loss drugs in the past. Besides Lorcaserin, Arena has other clinical candidates (Insomnia, Diabetes) that add value to the company.

By the end of this year, Arena is expected to have around $200 million in cash. Lorcaserin is not scheduled to be on the market until 2010 with expected revenues of $200 million in that year based on royalties from sales and anticipated milestone payments from a partner. With an 7X multiple, the valuation should be around $1.4 billion in 2010. Discounting this value by 30%, I get a valuation of about $800 million. I add about $400 million to valuation for it’s pipeline and cash on hand to get a valuation of $1.2 billion in 2007 or $26.1/share. Today, the stock is trading at $17.39 at a valuation of $823 million which is 50% below my estimated 2007 target. I am going to begin opening a position in this stock immediately! Of course, with the recent run-up there is a risk of a pull back which should be aggressively bought as well.

JMHO